Caterpillar Inc: Part 3 - The valuation & my strategy

What price should I catch this caterpillar before it turns into a butterfly and fly away?

*For the business model of Caterpillar Inc, please head over here for Part 1.

*For the financial and competitor analysis of Caterpillar plc, please head over here for Part 2.

At one time CAT 0.00%↑ share prices surged up to 7% after I started penning my thoughts on the company.

For a Dividend Aristocrat, with a sustainable dividend growth strategy, Cat might be trading at lesser than 20x P/E, which looks cheap, at 17x P/E. However do remember that it operates in a rather cyclical business, although downturns rarely last more than 3 fiscal years.

I will try to appraise Cat’s valuation using a few models, and then proceed to my strategy.

Price to earnings ratio

There are plenty of sources to get the P/E ratios.

Below is the 7-year historical P/E band of Caterpillar.

Why 7 years? Well remember about the sub-mine crisis in 2016? Caterpillar did slid into losses, so the P/E bands got distorted.

And also during the COVID affected fiscal years, where profits dipped while prices did not dipped as much or recovered faster with everything baked in.

So by just looking at historical P/E bands, anything touching 10x is cheap, while prices hitting 20x is expensive.

Assuming we pay a fair price, it would be ~16x P/E. With its latest EPS at $22.05 per share, fair valuation translates to $352.8.

With a 15x P/E, we are looking at $331.

Price to earnings growth ratio

Cat has a 20.3% CAGR EPS growth across the last 10 years.

Assuming if that holds true, its PEG ratio is 0.75x.

Keen eyed observers might have noticed that its latest EPS YoY growth is just around +10%.

Discounted cash flow

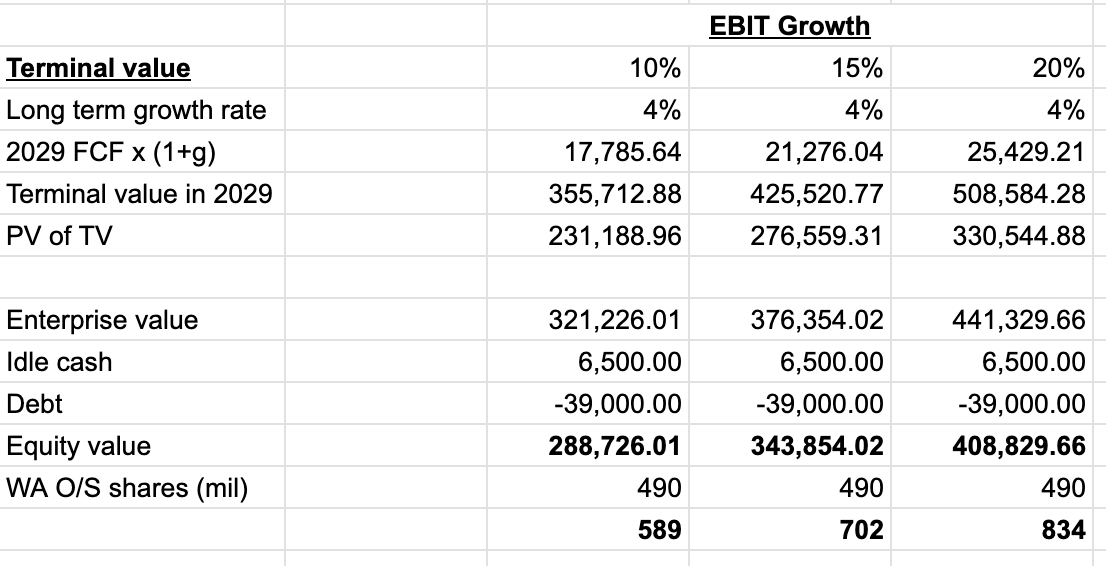

I decided to run 3 scenarios, assuming EBIT of Cat grows by 10%, 15% and 20%.

I used a 9% discount rate and a long term growth rate of 4%. Like LIN 0.00%↑, Cat tends to be stable and predictable

Below is the metrics for DCF for annual growth rates of 10%, 15% & 20%.

With CAT 0.00%↑ closing at around $350 per share, it looks like the company is undervalued, judging by DCF model, the fair value for Cat even growing its EBIT at 10% is $589 per share.

Dividend yield

Since Cat is a dividend stock, I thought we could use dividend yield as a pulse check of its valuation as well.

Historically, there are 2 instances when Cat traded at more than 4% dividend yield - one during the 2016 sub-mine crisis and another during the COVID-19 selloffs.

Total dividends paid out have increased, while there is an also visible trends of share buybacks.

All of these are done within its total cash generation from its business, a sign of prudence and sustainability.

I would take the dividend yield with a pinch of salt, rather than waiting for the next crisis to scoop up Cat.

As of now, it trades at just around 1.6% trailing dividend yield.

Even if we were to target a 2% dividend yield, we would be waiting for a price correction to a level of $276.5 per share, using $5.53 as its latest trailing dividend per share for FY 2024.

Recap

Price to earnings ratio of 15x = Target purchase price of $331

Discounted cash flow based on EBIT 10% growth rate = Fair value price of $589

Dividend yield of 2% = Target purchase price of $276.5

Strategy

I would be looking to initiate a long position on Cat if prices touch $ 320-$330 per share. As current share prices are around $350, we are looking at a possibility of a sudden one day crash or a few days of repeating corrections.

It could be a deployment by 1-2 tranches, or a lump sum deployment.

DISCLAIMER

The information available in this article/report/analysis is for sharing and education purposes only. This is neither a recommendation to purchase or sell any of the shares, securities, or other instruments mentioned; nor can it be treated as professional advice to buy, sell or take a position in any shares, securities, or other instruments. If you need specific investment advice, please consult the relevant professional investment advice and/or for study or research only.

No warranty is made concerning the accuracy, adequacy, reliability, suitability, applicability, or completeness of the information contained. The author disclaims any reward or responsibility for any gains or losses arising from the direct and indirect use & application of any contents of the article/report/written material.