Mapletree Pan Asia Trust 1H FY24/25: Unacceptable for a blue-chip REIT

The merger with MNACT looks to be a bad choice. I am halfway through eating my words

If I am ever to asked to write a book on how REIT managers should run a REIT well, I would definitely look at Link REIT (HKG: 0823) as the gold standard.

The unit price of Link might not be reflecting the inputs and efforts of the REIT manager, but when I had the opportunity to read up both Link and MPACT’s investor relations presentation, I start to see great disparity.

Don’t get me wrong, both MPACT and Link are definitely cream of the crop. But if I were to choose one as top and world class, it would have to be Link.

We are now slowly approaching the 3-year mark of the merger between MCT and MNACT. Previously I had been a vocal champion for the merger to take place. But as we slowly inch towards the full 3-year mark with little to no signs of synergism, accretive returns, and worse still, with even more risks, I can’t help but to slowly move towards the camp acknowledging the MNACT merger looks to be a bad decision.

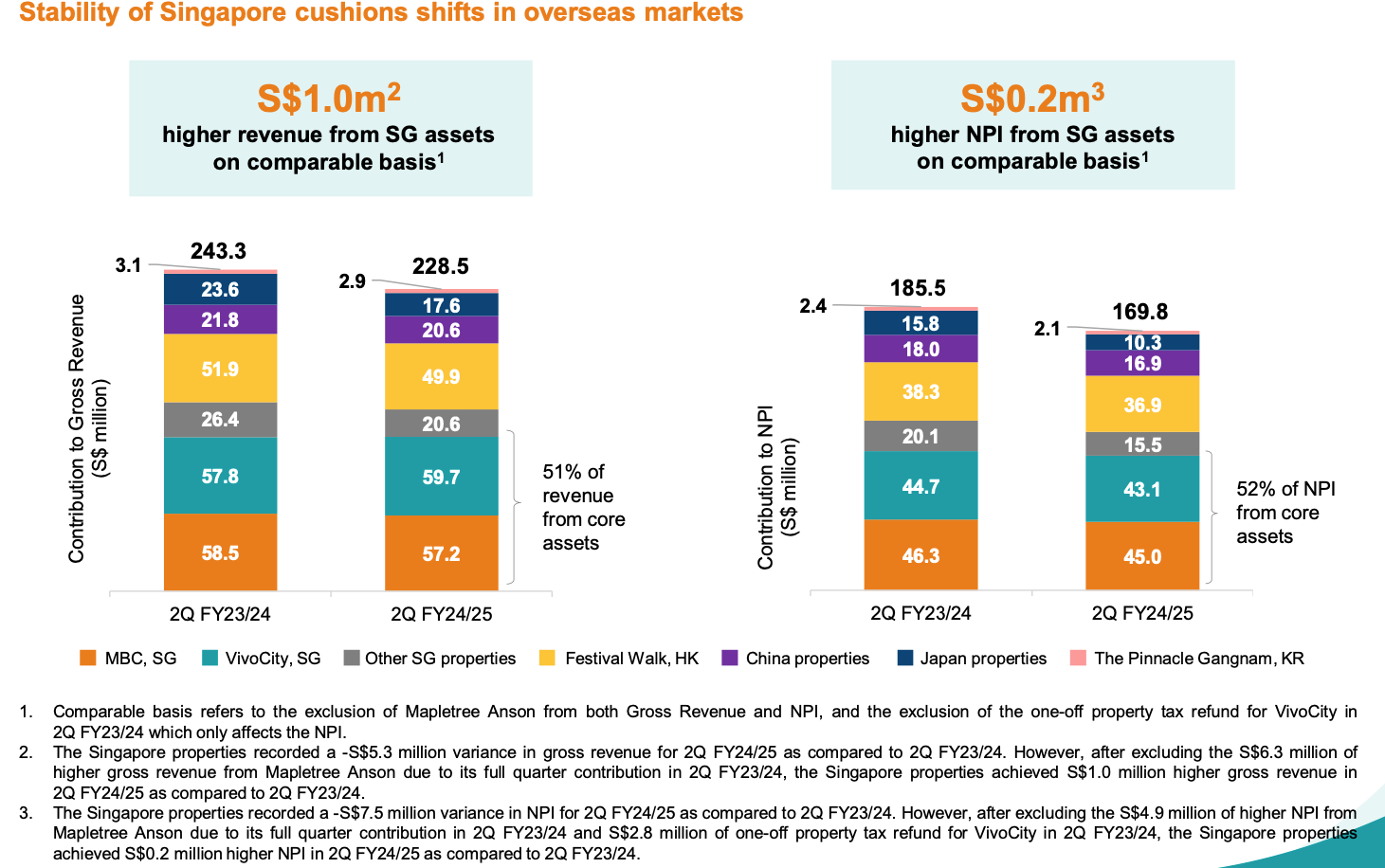

Enough of the emphasis of the SG core properties

Prior to the merger, I have no qualms of MCT highlighting its key core properties - VivoCity and MBC. But back when the merger was initiated, there was so much emphasis on how the merger would make MCT more diversified, opening up more geographical growth opportunities.

And let’s not forget MNACT was doing relatively well, albeit trading at a discount due to foreign currency and property risks.

But post merger, even as the North Asia properties were reeling from the extended impact of COVID-19, the REIT manager choses to distance itself from the contribution of North Asia’s properties, albeit also significantly making up 50% of the rest of its revenue and net property income.

Any investor would know and are aware of how VivoCity and MBC are the foundation and cornerstones of MPACT. I see the repeating highlights on how the core assets are contributing to MPACT’s results an effort to distance the underperforming North Asia assets.

So if the merger had worked well, am I expected to see another “curly bracket” highlighting “XX% of revenue and NPI from North Asia assets”?

I think investors are more anxious on what remedial actions are there if North Asia properties continue to drag MPACT down more in the coming quarters.

And it’s also a bit worrying seeing MBC’s contribution also shrinking instead of growing.

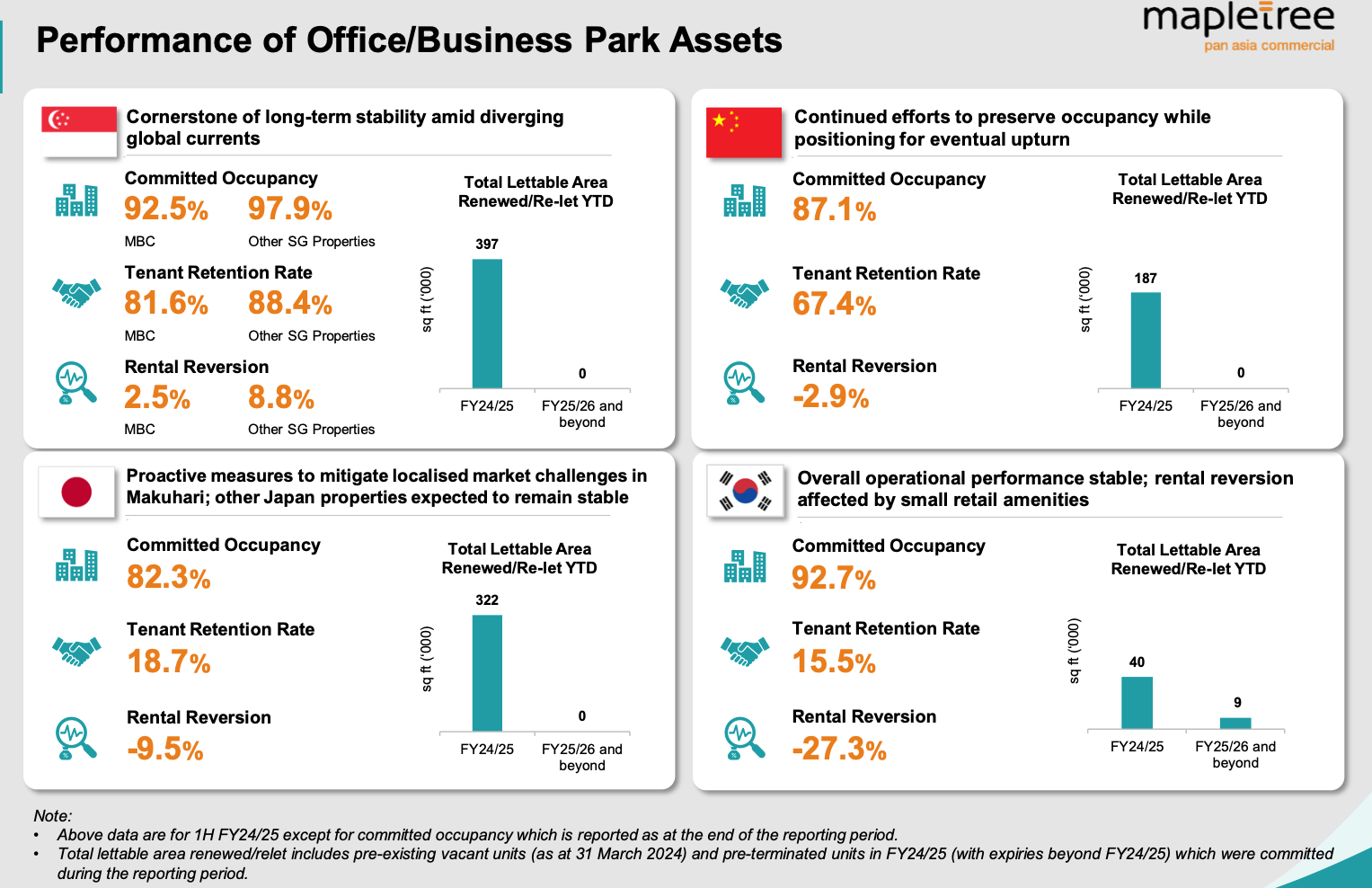

Meltdown of North Asia assets

I remember print screening this and sharing it across to my investing group, remarking “totally unacceptable!”

I never expected to see tenant retention rates lower than 70% for a blue-chip REIT.

The North Asia assets are slowly showing their weakness. On top of low tenant retention, some as astonishing as 15.5% and 18.7%, rental reversions have also nose-dived.

We are at 3 years post-pandemic peeps! This could have happened during the height of the pandemic, with the REIT managers admitting that they are sitting ducks. Although I can emphasise that economies in China and Japan aren’t necessarily booming, but that does not mean these properties should be allowed such results.

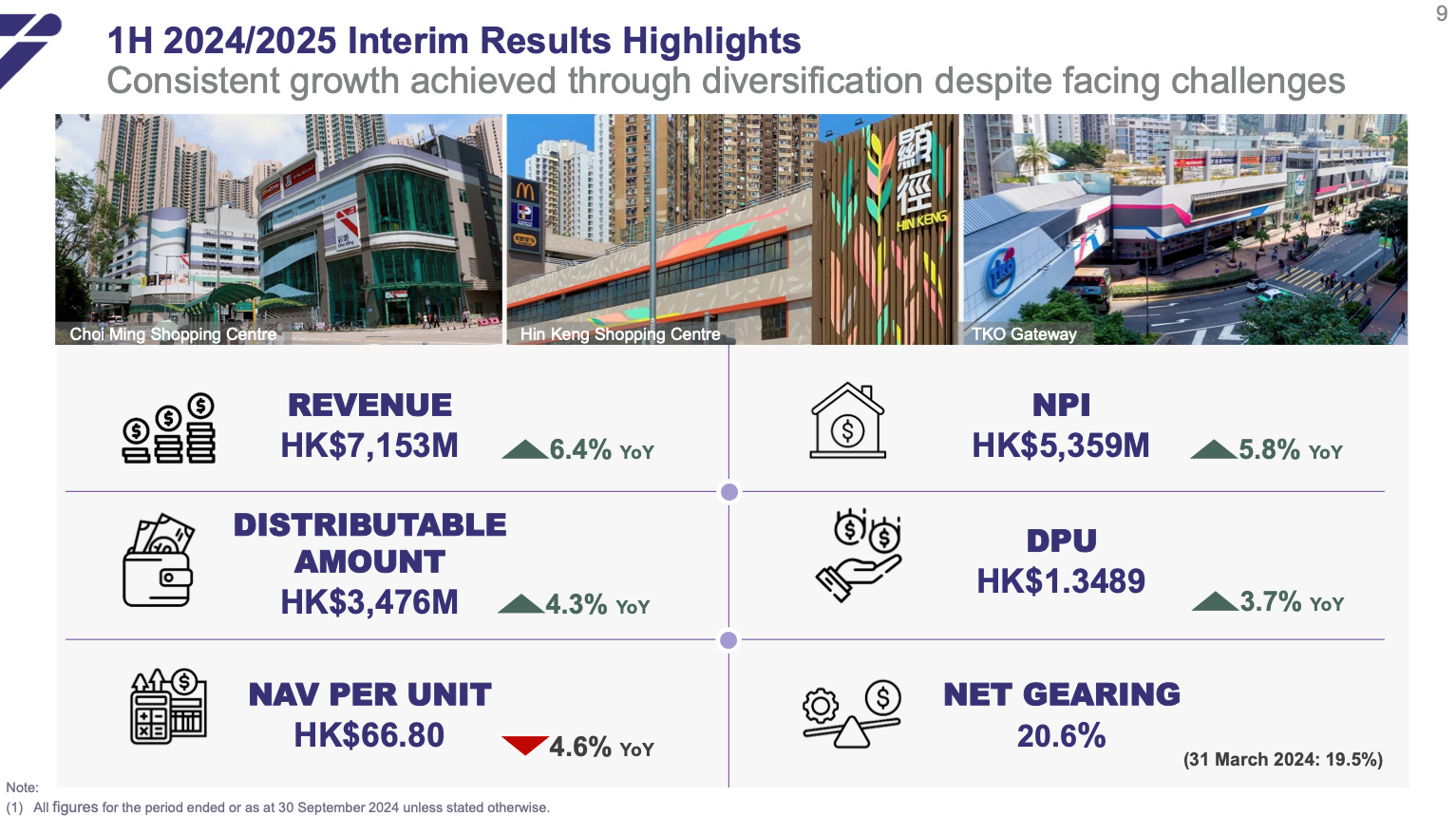

What could have been done better? Here’s a snippet of how Link REIT manages its non-renewing tenant and space.

The above is an example of how REIT managers can be more proactive in anticipating tenant non-renewal intent or even early termination requests. Within the span of 2 years, after Carrefour downsized its space, the previous space was redeveloped into a diversified trade mix space.

And within another year when Carrefour triggered early termination, the whole space was renovated and revamped to yield an ROI of 43.8%.

It might not be easy from an entire building perspective, but with REIT managers taking home a paycheque in the regions of millions, the expectation is that pro-activism should be inherent and not a choice.

Verdict

Not only gross revenue and net property income came in lower, the fair value loss on its properties meant that MPACT missed everything for 1H FY24/25.

And with MBC also showing a break in momentum, with potentially no near term recovery for the North Asia assets, it is no wonder unit price went back down to S$ 1.2-ish.

The Mapletree REIT managers have been piggybacking on their reputable sponsors and the indomitable strength of SG properties.

Perhaps they should learn to take a leaf out of Link REIT’s playbook to play their role much more proactively.

If a HK-centric REIT, still facing uncertain headwinds can still grow its revenue, NPI and DPU, I don’t see or accept why an S-REIT which has 51% of its revenue derived from 2 of the most coveted investment properties in Singapore should be doing worst.

Unacceptable for a blue chip REIT!

And I hope that MPACT makes me eat my words 6 months down the word.